Most families hear about FAFSA sometime during junior or senior year of high school.

Some students think it sounds confusing. Some parents assume it is only for families with very low incomes. Others worry that filing FAFSA means they are automatically signing up for student loans.

That confusion can cost families real money.

FAFSA stands for the Free Application for Federal Student Aid. It is the main form students use to apply for federal financial aid for college or career school. FAFSA information may also be used by states and colleges when awarding certain grants, scholarships, work-study, and other forms of aid.

The big idea is simple:

If college costs matter to your family, filing FAFSA should be part of the plan.

What FAFSA Is

FAFSA is the form that helps determine whether a student qualifies for different types of financial aid.

That aid may include:

- Federal grants

- State grants

- College-based aid

- Work-study

- Federal student loans

The word “loan” often makes families nervous, but FAFSA is not only about borrowing money. Filing FAFSA does not mean a student has to accept loans. It gives the student and family more information and more options.

A better way to think about FAFSA is this:

FAFSA is a key that can unlock financial aid options.

Some families will qualify for grants. Some may qualify for work-study. Some may use FAFSA to get a clearer picture of college costs. But without filing, families may never know what aid was available.

Why Filing FAFSA Matters

One of the biggest reasons to file FAFSA is that it can help students access money they do not have to pay back.

FAFSA can connect students to federal, state, and often college-based grants and scholarships. Examples may include Pell Grants, state grants, and institutional aid from colleges.

That matters because college pricing can be confusing.

A college may list one price on its website, but the amount a family actually pays may be different after grants and scholarships are applied. FAFSA can help colleges calculate aid and give families a more realistic view of the cost.

Families should not assume they will not qualify.

Even if a family thinks income is too high, assets are too complicated, or scholarships are already in place, filing FAFSA may still be worth it.

FAFSA Is Not Just About Loans

A common myth is that FAFSA is only for student loans.

That is not true.

FAFSA may help with:

- Grants: Money that generally does not need to be repaid.

- Scholarships: Some colleges use FAFSA information when awarding need-based scholarships.

- Work-study: A campus job program that can help students earn money while in school.

- Net price clarity: A better picture of what a college may actually cost after grants and scholarships.

- Federal student loans: If a student does borrow, federal student loans usually offer protections and terms that private loans may not.

The key point is that FAFSA gives families options. A student can file FAFSA, review the aid offer, and then decide what to accept or decline.

What FAFSA Can Help Unlock

Pell Grants

The Pell Grant is a major federal grant for students with financial need. Because it is a grant, it generally does not need to be repaid.

State Grants

Many states use FAFSA information to decide who qualifies for state financial aid. Missing FAFSA can mean missing state aid deadlines or opportunities.

Institutional Aid

Colleges may use FAFSA information to award their own need-based aid. That means the form can matter even if the money is coming from the college rather than the federal government.

Work-Study

Work-study can help students earn money through a campus job. These jobs are often designed to fit around a student’s class schedule.

Federal Student Loans

Families do not have to accept loans just because they file FAFSA. But if borrowing becomes necessary, federal loans may offer better terms and protections than private loans.

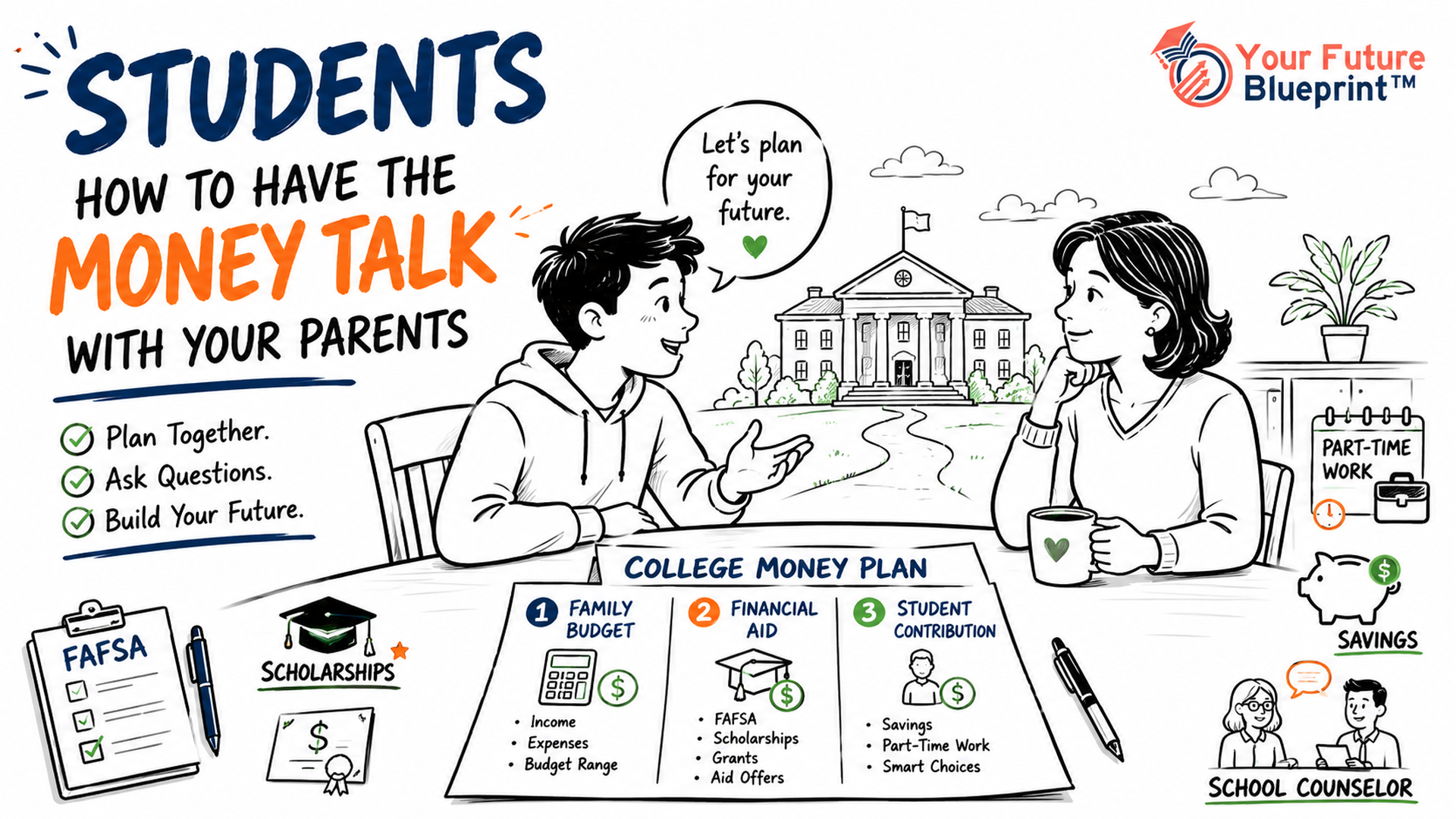

When and Where to File

Families should file FAFSA as early as possible once it becomes available for the school year.

The official place to file is StudentAid.gov. Families should avoid websites that charge money to submit FAFSA. The first word in FAFSA is Free for a reason.

Students and parents may each need their own StudentAid.gov account. For dependent students, parent information is usually required, and situations involving separated or divorced parents may require extra care when determining which parent provides FAFSA information.

Simple FAFSA Filing Checklist

Before senior year, families should:

- Create or confirm StudentAid.gov account access.

- Know the student’s Social Security number if applicable.

- Gather the required tax information.

- Make a list of colleges to receive FAFSA information.

- Review state and college FAFSA deadlines.

- File as early as possible once FAFSA opens.

- Read financial aid offers carefully before making a college decision.

- Ask the high school counselor or college financial aid office for help if something does not make sense.

Best Next Step

Do not wait until the last minute.

Even if your family is not sure whether you will qualify for aid, file FAFSA and review the results. It may unlock grants, scholarships, work-study, or better loan options. At a minimum, it gives your family a clearer picture of the real cost of college.

For more step-by-step help, visit the free Financial Aid Track:

Start the Free Financial Aid Track

Final Takeaway

FAFSA is not just paperwork.

It is one of the most important steps families can take to understand college costs and financial aid options.

Filing FAFSA does not force a student to borrow money. It does not mean the family has failed financially. It simply opens the door to possible aid and better information.

If college is on the table, FAFSA should be on the checklist.

Your future should not be limited by confusion, paperwork, or missed deadlines.

Sources & References

Federal Student Aid — FAFSA Form

https://studentaid.gov/h/apply-for-aid/fafsa

Use for the official FAFSA application and filing process.

Federal Student Aid — Types of Federal Student Aid

https://studentaid.gov/understand-aid/types

Use for the main types of federal student aid, including grants, loans, work-study, and scholarships.

Federal Student Aid — FAFSA Deadlines

https://studentaid.gov/apply-for-aid/fafsa/fafsa-deadlines

Use for federal, state, and college FAFSA deadline information.

Federal Student Aid — FAFSA Checklist: What Students Need

https://studentaid.gov/articles/things-you-need-for-fafsa/

Use for what students and contributors may need before starting the FAFSA, including StudentAid.gov accounts and required information.

Federal Student Aid — Completing the FAFSA Form: Steps for Parents

https://studentaid.gov/articles/fafsa-for-parents/

Use for parent contributor steps, parent information, and how schools and states use FAFSA information for aid eligibility and offers.

Federal Student Aid — How To Evaluate Your Aid Offers

https://studentaid.gov/articles/evaluating-financial-aid-offers/

Use for understanding how families can compare aid offers and consider grants, scholarships, work-study, and loans.

National Association of Student Financial Aid Administrators — About Financial Aid

https://www.nasfaa.org/about_financial_aid

Use for a broader professional context on FAFSA as a starting point for applying for aid from multiple colleges and funding sources.

Last reviewed: May 2026

Disclaimer

This article is for general educational purposes only and is not financial, tax, or legal advice. FAFSA rules, dates, deadlines, and eligibility requirements can change. Families should confirm current information at StudentAid.gov and with each college’s financial aid office.