Why this conversation matters

Talking with your parents about college money can feel uncomfortable. It may involve income, savings, debt, family limits, or expectations no one has discussed yet.

But avoiding the conversation does not make college costs disappear.

A calm money talk can help students understand what their family may be able to contribute, what the student may need to cover, and which college options are realistic before deadlines create pressure.

Reviewed for: 2026 college planning and financial aid conversations

Last reviewed: July 2026 | Review type: Policy-sensitive

Quick Answer

The college money talk should start early, calmly, and respectfully. Ask about your family’s realistic budget, what support may be available, what you may need to contribute, and whether FAFSA or CSS Profile will be required. The goal is not to solve everything in one conversation. The goal is to start planning with fewer assumptions.

Key Takeaways

- Start before applications, aid deadlines, or enrollment decisions create pressure.

- Ask about budget, parent support, student contribution, FAFSA, and CSS Profile.

- Use “I” statements so the conversation feels like teamwork.

- Family support can vary, so explore scholarships, work, community college, and lower-cost options.

- School counselors and financial aid offices can help when the situation is confusing or sensitive.

Who This Is For

Students: Helps you start the money conversation without sounding demanding or unprepared.

Parents: Helps families talk about costs, limits, and expectations calmly.

Counselors: Can be shared with students who need a practical starting point.

How to Start the Conversation

Choose a calm moment. Do not begin during an argument or when someone is rushed.

You might say:

“I know talking about money can be uncomfortable, but college is coming up, and I want to understand how we can make a realistic plan.”

Or:

“I’m not asking for every answer today. I just want to start learning what we should think about.”

Use “I” statements:

- “I want to understand what options are realistic.”

- “I want to help with the planning.”

- “I want to know what I should be responsible for.”

- “I want to avoid surprises later.”

Then listen. Your parents may have concerns about bills, debt, savings, job changes, or other responsibilities.

Questions to Ask

You do not need to ask everything at once. Start with a few:

- What is our realistic college budget range?

- What kind of support might be available?

- What do you expect me to contribute?

- Are there schools or costs we should avoid?

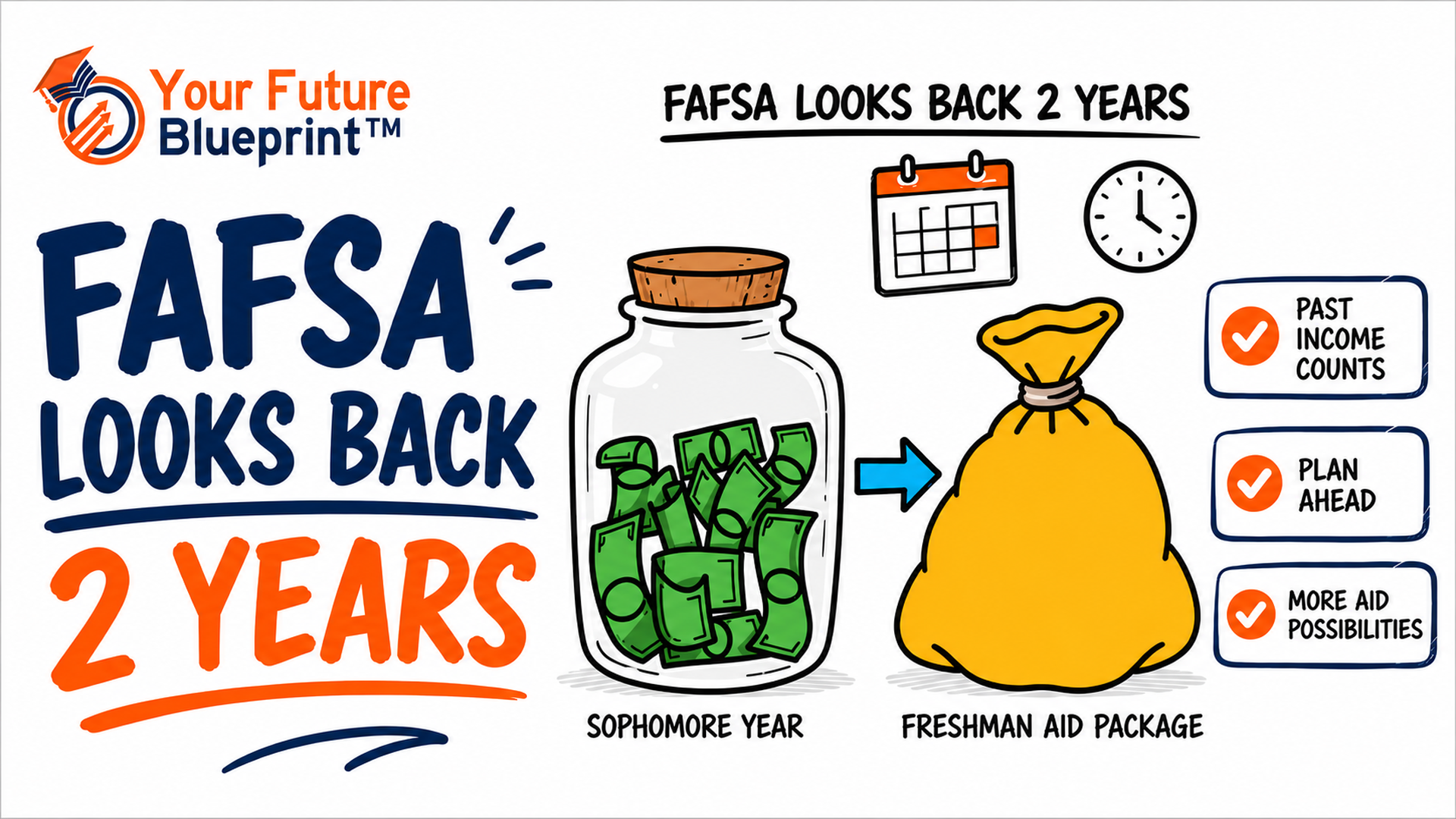

- Will we need to complete FAFSA?

- Will any colleges require CSS Profile?

- Who can help us review financial aid offers?

What Students Should Bring

Bring a short list of colleges or programs, estimated costs, FAFSA or CSS Profile questions, scholarship ideas, and a notebook for next steps. This shows you are trying to take ownership, not just asking your parents to solve everything.

Common Misconceptions

“Getting accepted means we can afford it.”

Acceptance and affordability are different.

“If my parents want me to go to college, they can pay for it.”

Many parents want to help but may have limits.

“Financial aid means free money only.”

Aid may include grants, scholarships, work-study, and loans.

“We only need one conversation.”

College money planning usually takes more than one talk.

What To Do If This Happens

If your parents do not want to talk right away

Stay calm and ask for a better time.

You can say:

“I understand this may not be a good moment. Could we pick a time this week to talk for 20 minutes?”

If your parents say they cannot afford much

That answer can be hard to hear, but it is still useful. It helps you build a realistic plan.

Next steps may include community college, in-state colleges, scholarships, part-time work, financial aid questions, or lower-cost career training options.

If your family situation is complicated

Some students have divorced or separated parents, limited contact with a parent, or a sensitive family situation. Do not try to solve everything alone. Talk with a school counselor, financial aid office, trusted adult, or official FAFSA support resource.

If your parent is worried about privacy

You can say:

“I understand this information is private. I’m not trying to judge or share it. I just want to understand what forms we need and what options are realistic.”

Use official websites and secure accounts. Do not share usernames or passwords.

If the conversation becomes tense

Pause and come back later.

You can say:

“I think this is getting stressful. Can we take a break and continue later?”

What To Watch For

- Do not assume your parents can or cannot pay.

- Check financial aid deadlines carefully.

- Review aid offers before accepting loans.

- Avoid shame, blame, or pressure.

- Use official websites and trusted adults for sensitive information.

Official / Trusted Links

Federal Student Aid — FAFSA Application

Use this official site to start or complete the FAFSA form.

Federal Student Aid — Completing the FAFSA Form: Steps for Parents

Use this page to understand parent and contributor steps for FAFSA.

Federal Student Aid — How to Add a Contributor to the FAFSA Form

Use this page if a parent, spouse, or other contributor needs to be invited to the FAFSA form.

College Board — CSS Profile

Use this official site to learn about CSS Profile for colleges and scholarship programs that require it.

U.S. Department of Education — College Scorecard

Use this tool to compare college costs, debt, graduation rates, and post-college earnings data.

What To Do Next

After the first conversation, write down:

- Family budget range

- Parent support available

- Student contribution expectations

- FAFSA next steps

- CSS Profile next steps, if needed

- Scholarships to research

- Colleges or programs to compare

- Questions for a counselor or financial aid office

Then schedule a follow-up conversation.

Best Next Step

Start with one calm conversation this week. Ask about the realistic college budget range, what support may be available, what you may need to contribute, and whether FAFSA or CSS Profile will be part of the plan.

Counselor Share Note

This article may be shared with students and families as a general educational resource. Families should still confirm details with official sources, school counselors, financial aid offices, college representatives, or trusted advisors.

Sources & References

Last Reviewed

July 12, 2026

Disclaimer

This content is for general educational purposes only and does not constitute financial, legal, tax, academic advising, or professional advice. Students and families should consult school counselors, financial aid offices, college representatives, official agencies, or trusted advisors before making final decisions.

View Transcript

Asking your parents about college money can feel awkward, but it is a conversation you should not skip.

Start early, choose a calm moment, and explain that you want to understand what options are realistic.

You might say:

“I know talking about money can be tough, but college is coming up, and I want to understand how we can make this work.”

Ask about your family’s budget range, what support may be available, what you may need to contribute, and whether FAFSA or CSS Profile is required.

Do not assume acceptance means affordability. Look at the full cost, financial aid, scholarships, work options, and lower-cost paths.

This is not a one-time conversation. It is the start of a plan. Follow up, take notes, and ask a school counselor or financial aid office for help when needed.

The talk may feel hard, but it can help you make smarter college choices with fewer surprises.

%20(1).png)