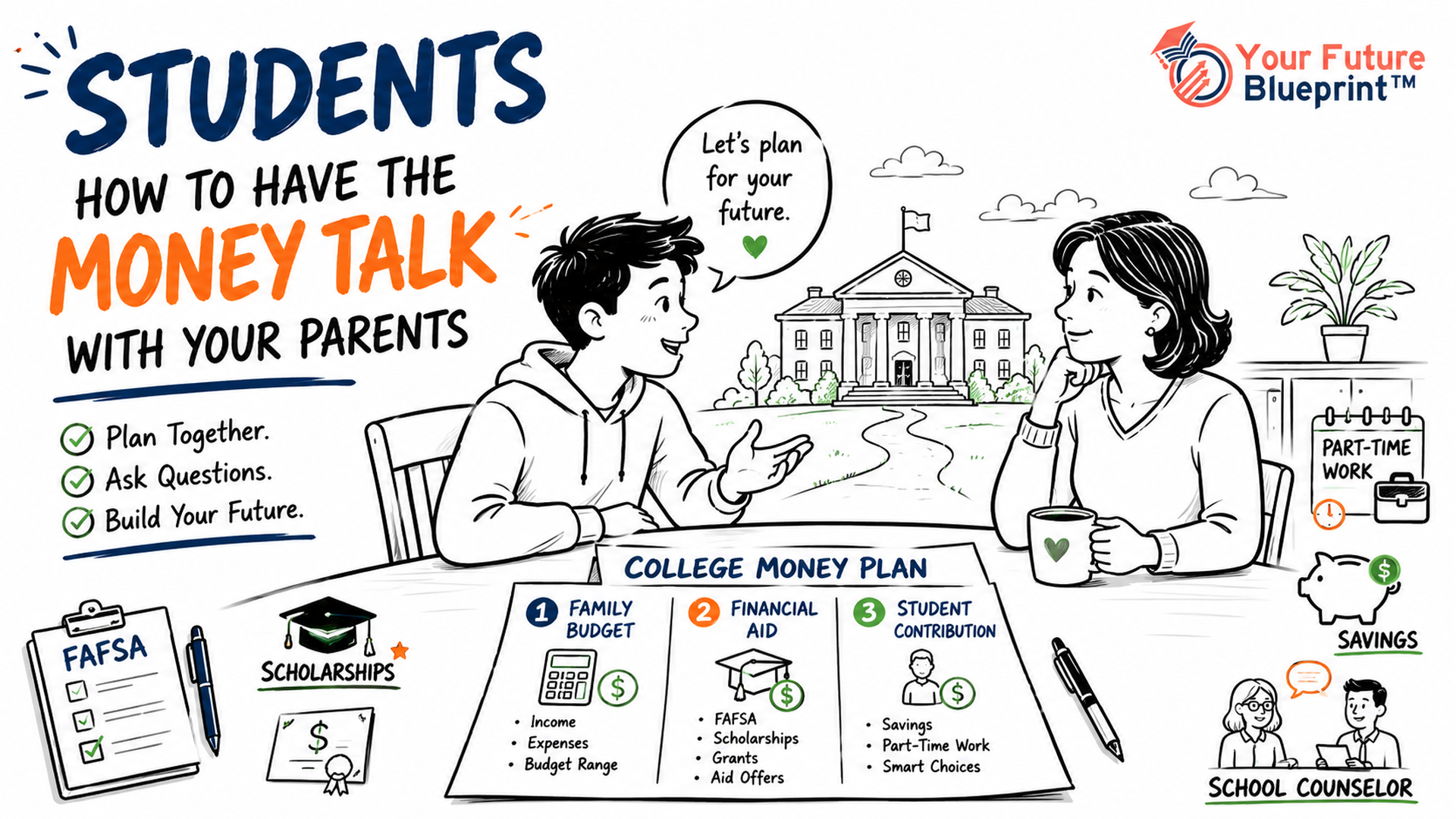

Many families consider the Free Application for Federal Student Aid (FAFSA) during senior year.

That makes sense. Senior year is when students are applying to colleges, comparing costs, and watching deadlines.

But here is the part many families do not realize early enough: some of the financial information used for FAFSA may come from earlier tax years. That means financial decisions made before senior year can matter later.

This does not mean families should panic. It also does not mean anyone should move money around without advice. It simply means that families should understand the rules early, ask better questions, and avoid accidental mistakes.

Quick Answer

FAFSA planning should start before senior year because aid eligibility can be affected by earlier tax information, account ownership, assets, and major financial changes.

Families should be careful with student-owned savings, understand how 529 plans and retirement accounts are treated, and talk with a financial aid office, tax professional, or financial advisor before making major decisions.

The goal is not to “game the system.” The goal is to plan honestly and avoid preventable surprises.

Why sophomore year may matter

FAFSA often uses tax information from an earlier year, sometimes called the “prior-prior year.”

For example, the 2026–27 FAFSA form uses 2024 income information.

That means a family’s financial picture before senior year may affect the aid calculation later.

This is especially important for families who may have:

- A large one-time income event

- A business sale

- An inheritance

- Major asset changes

- Student savings held in the student’s name

- College savings spread across different account types

- Retirement withdrawals or other taxable events

The main lesson is simple: if your student is in high school, FAFSA planning should not wait until the last minute.

Student-owned money can matter more

One common planning issue is money held in the student’s name.

In general, student assets are assessed differently from parent assets under the FAFSA formula, which can result in a greater effect on aid eligibility. The exact impact depends on the family's circumstances.

This does not mean students should never save money. Students should absolutely learn to save, budget, work, and manage money.

But families should understand that account ownership can matter. If a family is saving for college, it may be worth asking whether the money should sit in a student checking account, a parent-owned 529 plan, or another appropriate account.

The best answer can depend on the family’s situation, state rules, tax considerations, and financial goals.

529 plans can be useful, but families should understand ownership

A 529 plan is a tax-advantaged education savings account. Many families use 529 plans to save for college and other qualified education expenses.

For dependent students, parent-owned 529 plans are generally treated as parent assets on the FAFSA. That often has a lighter impact than money held directly in the student’s name.

Grandparent-owned 529 plans have also become a more attractive planning option under FAFSA simplification changes because distributions from those accounts are no longer reported as untaxed student income on the FAFSA.

Families should also consider any state tax benefits or state-specific rules that may apply to their 529 plan.

That does not mean every grandparent should open a 529 plan immediately. It means families should understand the option and ask informed questions.

Good questions include:

- Who owns the 529 account?

- Who is the beneficiary?

- How will withdrawals be timed?

- Are there state tax benefits or state-specific rules?

- Could this affect aid from a specific college?

- Should we talk with a financial advisor or tax professional first?

Be careful with large gifts to the student

Grandparents and relatives often want to help. That support can be meaningful.

But families should be careful about simply placing large gifts into the student’s bank account. Depending on timing and ownership, that money may show up as a student asset.

A better approach may be to talk through options before the gift is made.

For example, a family might ask:

- Should this gift go directly to the student?

- Should it go into a parent-owned 529 plan?

- Should a grandparent-owned 529 plan be considered?

- Should the gift be timed differently?

- Should the family talk with a tax professional first?

The key is to plan before money moves, not after.

Retirement accounts are treated differently

Qualified retirement accounts are generally not reported as FAFSA assets, although distributions and other tax consequences may affect future aid calculations depending on when they occur.

That is important because families sometimes worry that every dollar they have saved will count the same way. Retirement savings are different from regular savings, checking accounts, or other reportable assets.

But there is an important caution: taking money out of retirement accounts can create income or tax consequences. A withdrawal may affect future FAFSA information, taxes, penalties, retirement security, or other financial planning goals.

So the message is not “use retirement money for college.”

The better message is:

Do not make retirement or college funding decisions without understanding both the FAFSA and tax impact.

Timing large financial moves can matter

Some families have unusual financial events during high school years.

Examples may include:

- Selling a business

- Receiving an inheritance

- Selling investment property

- Taking a large retirement withdrawal

- Moving assets between accounts

- Receiving a major bonus or one-time income payment

If these events occur during the tax year used for the FAFSA or otherwise affect information reported on the application, they may influence the Student Aid Index (SAI) or a college's financial aid review. The impact varies depending on the type of event and individual circumstances.

Families cannot always control timing. Life happens. Jobs change. Businesses sell. Family members pass away. Expenses come up.

But when timing is flexible, it may be worth asking questions before making a large move.

When circumstances change, ask about professional judgment

Sometimes the financial information reported on the FAFSA does not reflect the family’s current situation.

For example, a family may have had higher income in the tax year used by FAFSA, but then a parent lost a job later. Or a family may have unusual medical expenses, business changes, or other financial circumstances.

In some situations, a college financial aid office may be able to review special circumstances through professional judgment.

Professional judgment decisions are made by individual colleges based on federal guidance and institutional procedures.

Professional judgment is not automatic. It does not guarantee more aid. It usually requires documentation, and each college may have its own process.

But it is still worth asking the financial aid office:

- Do you have a special circumstances process?

- What documentation do you need?

- Can you review a change in income?

- Can you review unusual expenses or one-time events?

- What deadlines should we know?

FAFSA planning is not about tricks

FAFSA planning should not be about hiding information, moving money dishonestly, or trying to beat the system.

It should be about understanding the rules before mistakes happen.

A family can plan honestly and still be strategic.

That might mean:

- Keeping college savings in an appropriate account

- Avoiding large student-owned balances when another structure makes more sense

- Understanding how 529 plans are treated

- Avoiding unnecessary retirement withdrawals

- Thinking carefully about the timing of large financial events

- Keeping documentation for unusual circumstances

- Contacting college financial aid offices early

What families should do next

If your student is a sophomore or junior, start with a simple family review.

You do not need a complicated spreadsheet. You just need to understand where things stand.

Ask:

- What accounts are in the student’s name?

- What accounts are in the parent’s name?

- Is there a 529 plan?

- Are grandparents or relatives planning to help?

- Are any large financial events expected before college?

- Has family income changed recently?

- Do we need advice from a tax professional, financial advisor, or financial aid office?

Then write down your questions and bring them to the right person.

A school counselor can help with planning and deadlines. A college financial aid office can explain how that college handles aid questions. A tax professional or financial advisor can help with account, tax, retirement, and estate planning questions.

What parents should remember

Parents do not need to know every FAFSA rule perfectly.

But they should know enough to avoid big surprises.

A helpful mindset is:

Before moving money, ask how it could affect college aid, taxes, and long-term family goals.

That one habit can prevent confusion later.

What students should remember

Students should not feel guilty for having savings, working a job, or trying to help pay for college.

Those are good habits.

But students should also understand that college financial aid forms look at accounts and income in specific ways.

If you have money saved in your name, ask a parent, counselor, or trusted adult whether that could affect aid planning.

You are not expected to figure this out alone.

What counselors and advisors should know

This topic can be sensitive because it touches on family finances, tax planning, retirement savings, gifts from relatives, and financial aid eligibility.

A counselor-friendly approach is to encourage families to start early and ask the right professionals. Counselors do not need to give tax or investment advice.

They can help families understand that FAFSA is not just a senior-year form and that early planning questions may matter.

Helpful language might be:

“FAFSA uses specific financial information, and some planning questions are best asked before senior year. If your family expects a major financial change, it may be worth talking with a financial aid office or financial professional.”

Best next step

If your student is still a sophomore or junior, use this year to get organized.

Look at where college savings are held. Ask whether relatives plan to help. Think about whether any major financial changes are coming.

Then talk with trusted professionals before making large decisions.

Your school counselors, teachers, and trusted mentors are a great place to start. If you want extra tools to stay organized, Your Future Blueprint can help you keep moving forward with more confidence.

Ready for the next step? Explore the recommended track for step-by-step guidance:

Keep learning

For more step-by-step FAFSA guidance, visit the Financial Aid track in Your Future Blueprint.

Sources & References

Last Reviewed

May 11, 2026

FAFSA rules and guidance can change from year to year. This article reflects federal guidance available as of May 11, 2026. Families should verify current requirements with Federal Student Aid and their college's financial aid office before making financial decisions.

Disclaimer

This content is for educational purposes only and does not constitute financial, legal, tax, investment, or professional advice. Students and families should consult with school counselors, financial aid offices, college representatives, financial advisors, accountants, or trusted advisors before making final decisions.

Families should consult a financial advisor or tax professional before making changes to retirement, estate, savings, or college funding plans.

No personal student information is collected or stored when accessing free content through verified K–12 school platforms. Any optional tools that collect user-provided information should be reviewed with the platform’s Privacy Policy and Terms of Use.