FAFSA Planning Moves You’ll Wish You Knew Two Years Ago

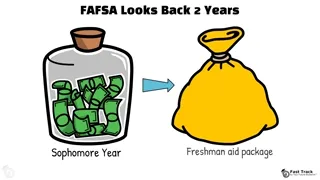

Here’s the hard truth: FAFSA does not look only at today. It often looks back two years at your tax returns and assets. That means the financial moves you make during your student’s sophomore year can directly affect their freshman aid package.

Families often realize this too late, but there are steps you can understand earlier.

One big mistake families make is keeping too much money in a student’s name. Money in a student account can count more heavily against aid than money held by a parent.

For example, $5,000 in a student savings account may affect aid differently than $5,000 in a parent-owned 529 plan. If you are planning ahead, it may make more sense to keep college savings in parent-owned accounts instead of leaving large amounts in the student’s checking or savings account.

Grandparent gifts also need planning. Many grandparents love helping with college costs, but a direct check to the student may create problems. A grandparent 529 plan may be a better option under current FAFSA rules.

Retirement accounts are another important area. Money inside certain retirement accounts is generally not counted as a FAFSA asset. But withdrawals from retirement accounts can show up as income later, which may affect aid.

Large financial moves can also matter. Selling a business, receiving an inheritance, making a large asset transfer, or taking a major distribution during the FAFSA lookback window can affect aid eligibility. If something unusual happens, families may need to document special circumstances and ask about an appeal.

FAFSA planning is not about tricks. It is about knowing the rules. Keep savings in the right accounts, use 529 plans wisely, understand retirement account rules, and plan at least two years ahead when possible.

Your high school sophomore’s financial picture may affect your future freshman’s aid package, so start learning now.

This content is for educational purposes only and does not constitute financial, legal, tax, or professional advice. Families should consult financial advisors, accountants, or financial aid professionals before making major decisions.

.png)